They sound and look complicated, but they’re not that bad, I promise. A W-4 is a tax form used by employers to withhold the correct amount of taxes from your paychecks. If you don’t fill out this form, or don’t fill it out correctly, you may end up having to pay additional taxes when you file your tax return at the end of the year.

Alternatively, if you request too much be taken out of your paychecks you might have a hard time paying your bills. Of course, you can change the allowance withheld from your paycheck as long as your employer allows you to. All you have to do is fill out another W-4.

What Is A W-4?

W-4s are also called “employee’s withholding certificate.”

It determines how much your employer will withhold from your paycheck. This withheld money gets sent to the Internal Revenue Service (IRS) on your behalf. Along with the cash for your taxes, your employer will send your Social Security number and your name so the IRS can track what money came from who.

The money sent to the IRS counts towards paying the annual income tax bill when you file your tax return in April. That’s why your W-4 asks for so much personal information.

You can also claim an exemption from withholding if you didn’t owe taxes last year and expect to not owe this year. This means that those income taxes won’t be taken out at all, though this is rare because the limits for taxable income are so low.

Related: What do I do if I lost my social security card?

When You Need To File A W-4

W4’s don’t get filed with the IRS. Instead, your employer will use the form to determine how much to take out of your checks for you. Once that’s done, they need to file it away somewhere for you – or them – to reference if any questions pop up.

You only have to fill out a W-4 if you start a new job or to make changes to the amount of taxes being taken out of your checks every week.

For example, if you realize you or are getting too much money taken out of your paycheck and want to reduce the taxes coming out. Or if you moved into a new tax bracket. This includes things like you got married or divorced, had a child, or got a second job.

You may also fill out a new W-4 if you want to withhold extra money from your paycheck for your next tax return. Your W-4 changes will take effect within the next one to three pay periods. Depending on how you’re paid.

So, if you think you’ll need to do this soon, it’s better to do it earlier than later.

How To Fill Out A W-4

The forms are easy to complete. But the numbers can seem overwhelming since they – logically – make no sense to anyone who doesn’t work at the IRS or in a tax office.

Your information:

Your name, address, filing status, and Social Security number. Your employer needs all this information so the IRS knows to apply the payment towards your income tax bill, not someone else’s. After completing this step, single filers with a simple tax situation only need to sign and date the form.

If you’re single, have no dependents, have only one job, and plan on filing a simple tax return, you can reasonably expect to always be a 0 on a W-4.

However, if that’s not you, there’s more math. First we’ll cover multiple jobs.

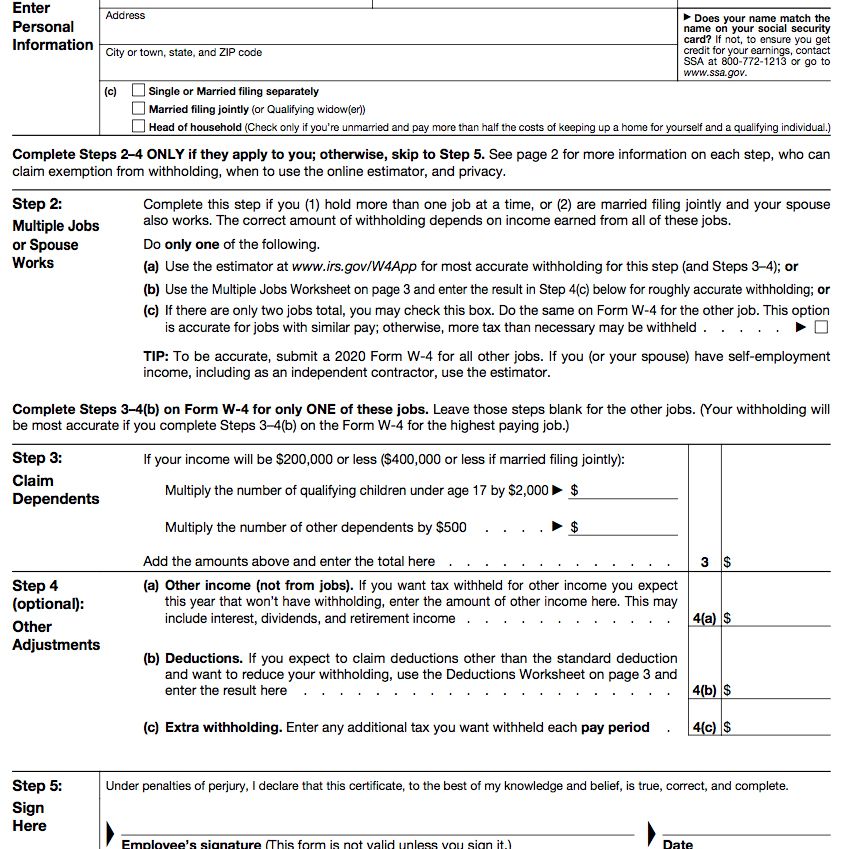

Multiple Jobs On W-4

If you have more than one job or your filing status is married filing jointly and your spouse also works, you need to figure out what number to put down. Since you’re filing jointly, this is considered two jobs if you both work. Which doesn’t make a ton of sense, but it’s the IRS, so…

Anyway, you have a few options to calculate your number:

Option 1:

Use the IRS’ online tax withholding estimator. This option has four steps that are basically the same as on the form itself, but it’s a bit easier if you’re getting jumbled on the math.

Option 2:

Fill out the multiple jobs worksheet. It’s provided on page three of the W-4 form. Enter the result from step 4C n the line. This is provided on the form your employer should have given to you. Alternatively, you can download the form from the IRS if they didn’t or you misplaced it.

The IRS advises the worksheet should only be completed on one W-4 form and the result should be entered for the highest paying job only.

For example, if your spouse makes more than you, use their income. Or if you have a full-time and a part-time job, use the income from whichever one makes more money. Not per hour, but overall.

Option 3:

Check the box in option C if there are only two jobs total. Do the same on the W-4 for the other job. Choosing this option makes sense if both jobs have similar pay period otherwise more tax may be withheld than necessary.

Dependents On W-4

If you have dependents, fill out step three to determine your eligibility for the child tax credit and credit for other dependents. This may also apply to lower-income families who may qualify for EIC.

Single taxpayers who make $20,000 or more or those married filing jointly who make less than $400,000 are eligible for the child tax credit, so you’re very likely to be eligible for the first one at least.

The IRS’ definition of a dependent is pretty complicated, but the short form is a qualifying person who lives with you and whom you support financially.

Multiply the number of qualifying dependents underage 17 by $2,000. Multiply the number of other dependents by $500. At the dollar sum of the two to line three. For example, if you have one of each dependent type, you will put $2,500 on line three.

Related: What is a legal dependent?

Additional Withholding W-4

Yeah, this may sound crazy. Especially given how much they’re already taking out of your paycheck. But the information you provided in the previous section might result in your employer withholding too little taxes over the course of the year.

If they withhold too little, you’ll end up having a big tax bill and possibly underpayment penalties and interest come April.

If you’re worried about this being the case, tell your employer to withhold extra money from each paycheck. If you overpay, you’ll get it back anyway.

The most likely cause of significant underholding is if you receive significant income on a 1099. This is a form used for interest, dividends, or self-employment income. No taxes are withheld from any of these income streams, so you’ll need to pay extra taxes to cover those.

You may also need to use this section if you’re still working but receive pension benefits from a previous job or Social Security retirement benefits.

Step four of the W4 allows you to have additional amounts withheld by filling out one or more of the three sections below:

4(a)

If you expect to earn non-job income such as dividends retirement accounts or savings enter the amount you expect to receive in this section.

4(b)

Fill out this section if you expect to claim reductions such as itemized reductions other than standard deductions and want to reduce withholding. Use the deduction worksheet provided on page three of the W4 form to calculate what to put here.

4(c)

This allows you to have any additional tax you want withheld from your paycheck. Including any amount from multiple jobs worksheet if this applies to you, but some people like to just use their tax return as a savings account. If that’s you, this is your line.

Sign & Dating

Signing and dating your W-4 is the easiest step. But it’s just as important as any other step. The form says, “Under penalties of perjury I declare I have examined this certificate and to the best of my knowledge and belief it is true, correct, and complete.”

You need to sign your name below that statement where it says employees’ signature. Then enter the date to the right. Your W-4 is not valid until you do so.

And, as a reminder, lying on this form is paramount to perjury which is punishable by jail time and sizable fines, so, you know, be honest about who you are and all that.

People like to fixate on the numbers, but, really, you can put whatever number down you want. It’s just generally not in your best interest to do so. When in doubt, go lower.

Half-Year Withholding

If you will be employed no more than 245 days of the year, request in writing that your employer use the half-year method to compute your withholding. The basic withholding formula assumes a full year of employment. Without using the part-year method, you’ll have too much withheld.

Of course, you’ll get your money back, but it’s still nice to have liquid assets on hand.